- 🩺 What Is Health Insurance?

- 💰 How Does Health Insurance Work?

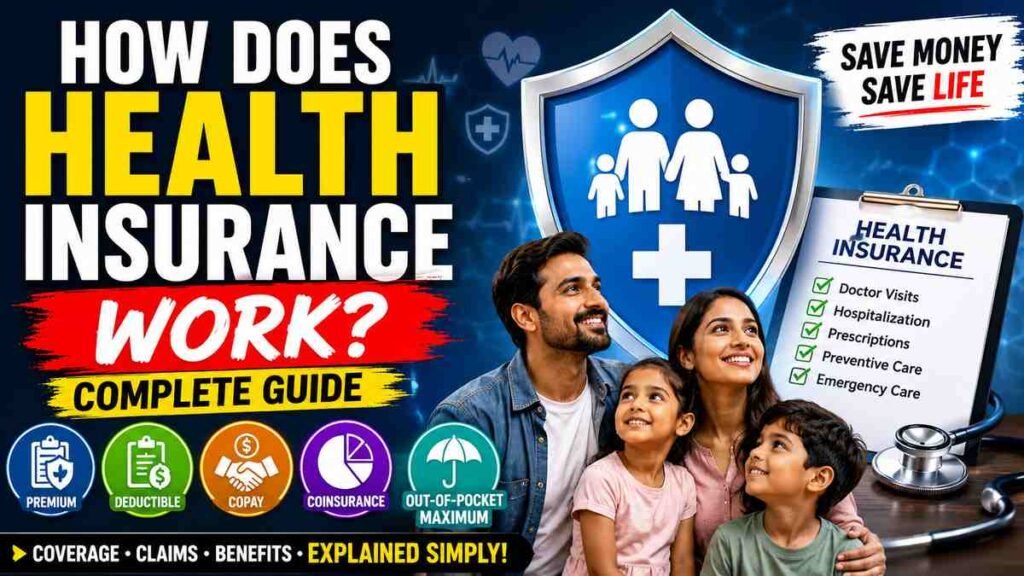

- 🧾 Understanding the Most Important Health Insurance Terms

- 🏨 How Health Insurance Pays Medical Bills

- 📄 What Is a Health Insurance Claim?

- 🏥 In-Network vs Out-of-Network Doctors

- 👨⚕️ Different Types of Health Insurance Plans

- 💊 What Health Insurance Usually Covers

- 🚫 What Health Insurance May Not Cover

- 🧠 Why Preventive Care Matters

- ⚠️ Common Health Insurance Mistakes

- 🏥 How to Choose the Right Health Insurance Plan

- ❤️ Why Health Insurance Matters So Much

- 🌟 Final Thoughts

- ❓ FAQs

Health insurance feels confusing for many people initially.

You hear terms like:

- Premium

- Deductible

- Copay

- Coinsurance

- Out-of-pocket maximum

…and suddenly it sounds like a complicated math problem instead of healthcare.

However, once you understand the core system, health insurance becomes much easier to navigate.

More importantly, understanding how health insurance works can protect you financially during medical emergencies, surgeries, accidents, chronic illnesses, and unexpected hospital visits.

⚠️ Without health insurance, even a short hospital stay can create massive financial stress.

Therefore, this complete guide will simplify everything step by step in plain human language.

By the end, you will understand:

- What health insurance actually does

- How claims work

- What premiums and deductibles mean

- How insurance companies make money

- What costs you still pay yourself

- How to choose the right plan

- Common mistakes people make

Let’s break it down simply.

🩺 What Is Health Insurance?

Health insurance is basically a financial protection system for medical expenses.

Instead of paying massive healthcare bills completely on your own, you and the insurance company share the costs.

Here’s the simple idea:

You pay a smaller predictable amount regularly.

Meanwhile, the insurance company helps cover expensive medical costs when you need healthcare.

⚡ Think of health insurance like a safety net.

Most people hope they never face:

- Major surgery

- Cancer treatment

- Emergency hospitalization

- Serious accidents

- Long-term illness

However, if those situations happen, health insurance prevents medical costs from becoming financially devastating.

💰 How Does Health Insurance Work?

At its core, health insurance works through risk-sharing.

Millions of people pay monthly premiums into the insurance system.

Most people remain relatively healthy during any given month.

Therefore, insurance companies use the pooled money to help pay medical costs for individuals who need expensive treatment.

📌 In simple words:

Everyone contributes regularly so nobody faces catastrophic healthcare costs alone.

🧾 Understanding the Most Important Health Insurance Terms

Many people feel overwhelmed because insurance companies use complicated terminology.

However, these concepts become easy once explained clearly.

💳 Premium: Your Monthly Payment

A premium is the amount you pay regularly to keep your insurance active.

Usually, you pay:

- Monthly

- Quarterly

- Or annually

Even if you never visit a doctor, you still pay the premium.

⚡ Think of it like a subscription fee for healthcare protection.

For example:

- You may pay $300 monthly for health insurance coverage

- Your employer may also contribute part of the premium

Generally:

- Lower premiums often mean higher out-of-pocket costs later

- Higher premiums usually reduce costs during medical treatment

🏥 Deductible: What You Pay First

A deductible is the amount you must pay yourself before insurance starts sharing costs.

For example:

- Suppose your deductible is $2,000

- You pay the first $2,000 of covered healthcare expenses

- Afterward, insurance begins contributing

Consequently, people with high deductibles often pay more upfront before insurance assistance begins.

💵 Copay: Fixed Small Payments

A copay is a small fixed amount you pay for specific services.

Examples include:

- $25 doctor visit

- $15 prescription

- $50 specialist appointment

Meanwhile, the insurance company covers the remaining approved amount.

Copays help simplify smaller healthcare costs.

📊 Coinsurance: Shared Percentage Costs

Coinsurance means you split healthcare costs with your insurance company after meeting the deductible.

For example:

- Insurance covers 80%

- You cover 20%

Suppose a medical bill equals $10,000.

After meeting the deductible:

- Insurance pays $8,000

- You pay $2,000

Therefore, coinsurance creates shared responsibility between both sides.

🚨 Out-of-Pocket Maximum: Your Financial Safety Limit

This is one of the most important protections in health insurance.

Your out-of-pocket maximum limits how much you personally spend during a policy year.

Once you hit that limit:

- Insurance covers 100% of covered services afterward

For example:

- Maximum = $8,000

- After paying $8,000 yourself, insurance handles additional approved expenses

⚡ This protection becomes life-changing during serious illness or hospitalization.

🏨 How Health Insurance Pays Medical Bills

Let’s walk through a real-world example.

Suppose you break your leg.

Here’s what usually happens:

- You visit the hospital

- The hospital sends the bill to your insurer

- Insurance reviews the claim

- Insurance determines covered costs

- You pay your required share

- Insurance pays the remaining approved amount

This process is called a health insurance claim.

📄 What Is a Health Insurance Claim?

A claim is simply a request for payment sent to the insurance company.

Usually:

- Hospitals submit claims automatically

- Doctors send treatment details

- Insurance companies review coverage eligibility

Then:

- Approved expenses get processed

- Remaining patient responsibility gets calculated

Consequently, you receive an explanation of benefits (EOB).

This document explains:

- What insurance paid

- What you owe

- Which services were covered

🏥 In-Network vs Out-of-Network Doctors

This distinction matters enormously.

Insurance companies negotiate discounted rates with specific hospitals and doctors.

These providers become “in-network.”

Therefore:

- In-network care costs less

- Out-of-network care costs much more

⚠️ Some insurance plans barely cover out-of-network services at all.

Consequently, checking provider networks before appointments saves significant money.

👨⚕️ Different Types of Health Insurance Plans

Not all insurance plans work the same way.

Here are the most common types.

🩺 HMO (Health Maintenance Organization)

HMOs usually:

- Cost less monthly

- Require primary care physicians

- Need referrals for specialists

However, they also limit provider flexibility more strictly.

🌐 PPO (Preferred Provider Organization)

PPOs offer:

- Greater flexibility

- Easier specialist access

- Better out-of-network coverage

However, premiums usually cost more.

⚡ EPO (Exclusive Provider Organization)

EPOs combine aspects of HMOs and PPOs.

They:

- Require network providers

- Usually avoid referral requirements

Meanwhile, costs often remain moderate.

💼 Employer-Sponsored Health Insurance

Many people receive health insurance through employers.

In these plans:

- Employers often pay part of the premium

- Employees pay remaining portions

- Coverage extends to dependents sometimes

Employer-sponsored insurance remains one of the most common healthcare systems globally.

🧓 Government Health Insurance Programs

Governments also provide healthcare programs for specific groups.

Examples include:

- Medicare

- Medicaid

- Veterans healthcare programs

- Public healthcare systems

Eligibility varies depending on:

- Age

- Income

- Disability status

- Country-specific regulations

💊 What Health Insurance Usually Covers

Coverage varies between policies.

However, many plans commonly cover:

- Doctor visits

- Emergency care

- Hospitalization

- Surgery

- Preventive screenings

- Prescription medications

- Laboratory tests

- Mental health treatment

Meanwhile, some plans include:

- Maternity care

- Physical therapy

- Vision benefits

- Dental benefits

Always review policy details carefully.

🚫 What Health Insurance May Not Cover

Many people mistakenly assume insurance covers everything.

Unfortunately, exclusions often exist.

Some policies may exclude:

- Cosmetic procedures

- Experimental treatments

- Certain medications

- Alternative therapies

- Elective surgeries

Additionally, some treatments require pre-authorization beforehand.

🧠 Why Preventive Care Matters

Many insurance plans heavily encourage preventive healthcare.

Therefore, insurers often fully cover:

- Vaccinations

- Annual physical exams

- Cancer screenings

- Blood pressure checks

- Cholesterol tests

Why?

Because prevention costs far less than treating advanced illness later.

Consequently, preventive care benefits both patients and insurers financially.

📈 Why Health Insurance Costs Keep Rising

Healthcare costs rise for many reasons.

Major factors include:

- Expensive medications

- Advanced technology

- Aging populations

- Administrative costs

- Hospital pricing

- Chronic disease increases

As healthcare costs rise, insurance premiums usually increase too.

⚠️ Common Health Insurance Mistakes

Many people accidentally create financial problems through avoidable mistakes.

❌ Choosing Plans Based Only on Premiums

Cheap monthly premiums may hide:

- High deductibles

- Massive out-of-pocket costs

- Limited networks

Always evaluate total potential costs.

❌ Ignoring Provider Networks

Using out-of-network hospitals can create shocking bills.

Always verify provider participation beforehand.

❌ Skipping Preventive Care

Preventive services detect problems early.

Ignoring them increases long-term health and financial risks.

❌ Not Understanding Coverage Details

Many people never read:

- Deductibles

- Coverage limits

- Exclusions

- Medication formularies

Consequently, surprises happen during emergencies.

🏥 How to Choose the Right Health Insurance Plan

Choosing the right plan depends on:

- Your budget

- Medical history

- Family size

- Prescription needs

- Preferred doctors

- Risk tolerance

Ask yourself:

- Do I visit doctors frequently?

- Do I need specialist care?

- Do I take regular medications?

- Could I handle large emergency bills?

Your answers help determine ideal coverage.

❤️ Why Health Insurance Matters So Much

Medical emergencies arrive unexpectedly.

Nobody plans for:

- Cancer diagnoses

- Car accidents

- Heart attacks

- Emergency surgeries

However, health insurance creates financial protection during vulnerable moments.

Without insurance:

- Debt increases rapidly

- Savings disappear quickly

- Financial stress intensifies dramatically

Therefore, health insurance protects both health and financial stability simultaneously.

🌟 Final Thoughts

Health insurance may feel confusing initially.

However, once you understand:

- Premiums

- Deductibles

- Copays

- Coinsurance

- Provider networks

…the system becomes far less intimidating.

Most importantly, health insurance exists to reduce financial devastation during medical crises.

Although no plan feels perfect, having coverage usually provides significantly greater protection than facing major healthcare expenses entirely alone.

Therefore:

- Learn your policy carefully

- Understand your costs

- Use preventive care

- Review networks regularly

- Ask questions whenever confused

Because informed healthcare decisions can protect both your health and your future finances.

❓ FAQs

❓ What is the main purpose of health insurance?

Health insurance helps reduce personal financial burden from medical expenses by sharing healthcare costs between patients and insurers.

❓ What happens if I don’t meet my deductible?

You continue paying covered healthcare costs yourself until reaching the deductible threshold.

❓ Are preventive services free with insurance?

Many insurance plans fully cover preventive care like annual checkups, vaccinations, and screenings.

❓ What is the difference between copay and coinsurance?

A copay is a fixed fee, while coinsurance is a percentage of healthcare costs.

❓ Why are out-of-network doctors more expensive?

Insurance companies negotiate lower rates with in-network providers, while out-of-network services often lack those discounts.

❓ Can health insurance deny claims?

Yes. Claims may get denied for reasons like non-covered services, missing documentation, or policy exclusions.

❓ Is employer health insurance better than private insurance?

Not always. Employer plans often cost less because employers contribute financially, but coverage quality varies widely.

❓ What is the out-of-pocket maximum?

It is the yearly limit on how much you personally pay for covered medical services before insurance covers 100% afterward.

Authoritative Source Links for the Blog

- Healthcare.gov – Official Health Insurance Information

- Centers for Medicare & Medicaid Services (CMS)

- Kaiser Family Foundation – Health Insurance Basics

- Mayo Clinic – Understanding Health Insurance

- Investopedia – Health Insurance Explained

- National Institutes of Health (NIH)

You may also like to read other health related articles here also authored by me :

Gym Herpes Outbreak? How to Stay Safe While Working Out

Can Apple Cider Vinegar Help Weight Loss Journey?

Mewing Explained: Does This Viral Jawline Trend Actually Work?

What Your Hands Are Warning You About Your Heart: Hidden Signs

Pingback: Americans, what is your worst healthcare story? - hospscout.com