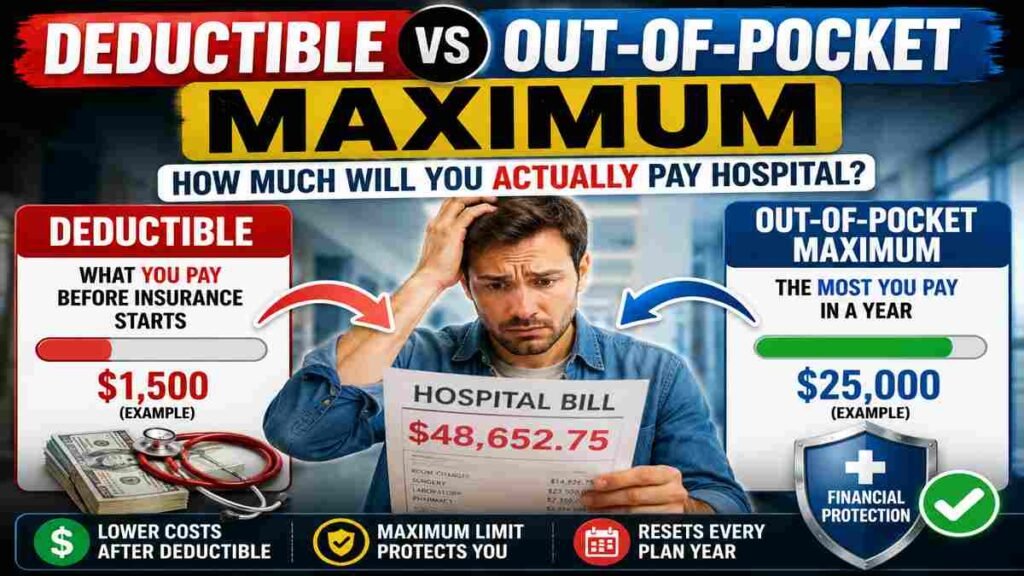

- 🏥 What Is a Deductible?

- 💰 What Is an Out-of-Pocket Maximum?

- ⚠️ Deductible vs Out-of-Pocket Maximum: The Key Difference

- 📋 Real-Life Scenario: How Hospital Bills Actually Work

- 🚨 What Happens If You Need Major Surgery?

- 🛡️ How the Out-of-Pocket Maximum Protects You

- 👨👩👧 Family Deductibles vs Family Out-of-Pocket Maximums

- ⚠️ Important Costs That May NOT Count

- 🧠 Why Hospital Bills Feel So Confusing

- 📊 Deductible vs Coinsurance vs Copay

- ⚡ How to Reduce Your Hospital Costs

- 🧭 Final Thoughts

- ❓FAQs About Deductibles and Out-of-Pocket Maximums

- Authoritative Source Links

Most people think health insurance means the insurance company pays everything. Unfortunately, that is not how it works. In reality, you usually pay part of the bill first through your deductible, copays, and coinsurance. However, once your total spending reaches your out-of-pocket maximum, your insurance typically starts covering almost all eligible medical expenses for the rest of the year.

Here’s the simplest way to understand it:

- Deductible = the amount you must pay before insurance starts sharing costs

- Out-of-pocket maximum = the absolute most you pay in a year for covered medical care.

So if your deductible is $1,500 and your out-of-pocket maximum is $25,000:

You first pay the deductible yourself

Then you share costs with insurance

Eventually, once your spending hits $25,000, insurance covers nearly everything else

Understanding this difference can literally save you thousands of dollars during hospital visits, surgeries, MRIs, or emergencies.

Now let’s break it down clearly with real-world examples and practical scenarios.

🏥 What Is a Deductible?

A deductible is the amount you must pay for covered healthcare services before your insurance company starts contributing.

Think of it as your “entry fee” into the insurance-sharing system.

For example:

- Your deductible = $1,500

- You receive hospital services worth $4,000

You usually pay the first $1,500 yourself before insurance starts helping with the remaining balance.

However, many plans still require:

- Copays

- Coinsurance

- Non-covered service charges

even after you meet the deductible.

💰 What Is an Out-of-Pocket Maximum?

Your out-of-pocket maximum is the financial ceiling on what you personally spend during a policy year for covered healthcare services.

Once you hit that limit:

- Insurance usually pays 100% of covered services

- You stop paying deductibles

- Coinsurance ends

- Most cost-sharing disappears

Therefore, the out-of-pocket maximum protects you from catastrophic medical debt.

For instance:

- Out-of-pocket maximum = $25,000

- You suffer a major illness requiring expensive treatment

After spending $25,000 on eligible care, your insurance should cover the rest for the remainder of the year.

⚠️ Deductible vs Out-of-Pocket Maximum: The Key Difference

Many people confuse these terms because both involve personal spending. Nevertheless, they work very differently.

| Feature | Deductible | Out-of-Pocket Maximum |

|---|---|---|

| What it means | Amount you pay before insurance shares costs | Maximum yearly spending limit |

| Happens when? | Early in coverage year | After major healthcare spending |

| Includes coinsurance? | Usually no | Yes |

| Includes copays? | Sometimes | Usually yes |

| Purpose | Cost-sharing trigger | Financial protection ceiling |

In simple words:

- Deductible starts cost-sharing

- Out-of-pocket maximum stops cost-sharing

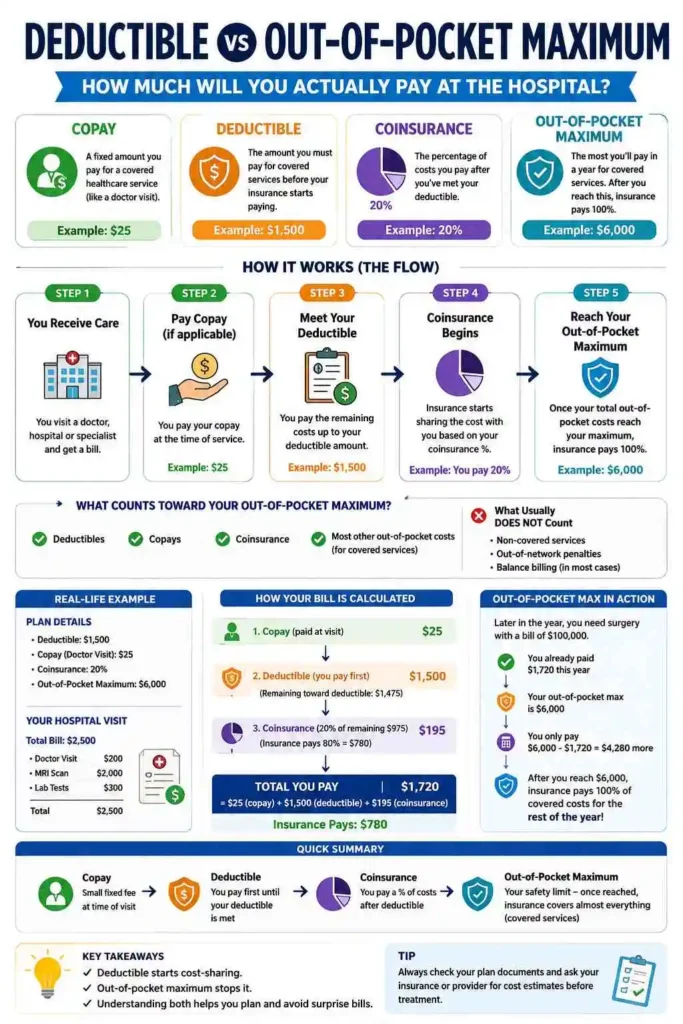

📋 Real-Life Scenario: How Hospital Bills Actually Work

Let’s use a realistic hospital billing example.

👨⚕️ Insurance Plan Details

Imagine your health insurance includes:

- Individual deductible: $1,500

- Family deductible: $3,000

- Out-of-pocket maximum: $25,000 per person

- Family out-of-pocket maximum: $150,000

- Doctor visit copay: $25

- MRI coinsurance: 20%

This means:

- You must personally pay the first $1,500 of eligible medical expenses each year

- Afterward, insurance starts sharing costs

- Eventually, after spending $25,000, your insurance covers nearly all additional covered services

🩻 Example Hospital Visit

Now imagine you visit the doctor on January 1st.

You receive:

- Doctor checkup

- MRI scan

- Radiology interpretation

Here are the costs:

| Service | Cost |

|---|---|

| Physician visit | $120 |

| MRI scan | $1,800 |

| Radiologist fee | $150 |

| Total | $2,070 |

💵 What You Actually Pay

🧾 Step 1: Copay

At the doctor’s office, you immediately pay:

- $25 copay

That payment usually does not count toward the deductible in some plans.

📄 Step 2: Coinsurance

Your insurance says:

- You owe 20% coinsurance for the MRI

20% of $1,800 MRI-eligible amount:

- $360

So now:

- You paid $25 copay

- Plus $360 coinsurance

💰 Step 3: Deductible Responsibility

Your deductible still applies to remaining eligible costs.

The remaining expenses include:

- Physician fee

- Radiologist fee

- Remaining MRI balance

Insurance processes claims based on the order providers submit them.

After calculations:

- You become responsible for approximately $1,500 deductible spending

- Insurance contributes toward the remaining covered amount

As a result:

- Your deductible becomes fully satisfied for the year

📉 What Happens After You Meet the Deductible?

This is where insurance finally becomes more valuable.

Once you meet your deductible:

- Insurance starts sharing more costs

- Your financial burden decreases

- You mainly pay coinsurance or copays

For example:

- Future MRIs may only require 20% coinsurance

- Specialist visits may only require copays

- Some preventive care may become fully covered

Therefore, reaching your deductible often significantly lowers your medical spending afterward.

🚨 What Happens If You Need Major Surgery?

Now imagine later that year you require:

- Heart surgery

- Cancer treatment

- Extended hospitalization

Your medical bills skyrocket to:

- $300,000

- $500,000

- Or more

At this stage, your out-of-pocket maximum becomes critically important.

🛡️ How the Out-of-Pocket Maximum Protects You

Suppose your maximum is:

- $25,000 individual

As you continue paying:

- Deductibles

- Coinsurance

- Copays

your spending accumulates toward that limit.

Once your total reaches $25,000:

- Insurance should pay 100% of covered services for the remainder of the year

That protection prevents complete financial devastation from catastrophic illness.

👨👩👧 Family Deductibles vs Family Out-of-Pocket Maximums

Many family plans contain two levels:

- Individual limits

- Family limits

For example:

- Individual deductible = $1,500

- Family deductible = $3,000

This means:

- One person may satisfy their own deductible

- Or multiple family members together may satisfy the family deductible

Similarly:

- Individual out-of-pocket maximum protects one person

- Family out-of-pocket maximum protects the household overall

⚠️ Important Costs That May NOT Count

This part surprises many patients.

Not every medical expense counts toward:

- Deductibles

- Out-of-pocket maximums

Usually excluded:

- Non-covered services

- Cosmetic procedures

- Out-of-network penalties

- Certain prescription categories

- Balance billing amounts

Therefore, always verify coverage carefully before major procedures.

🧠 Why Hospital Bills Feel So Confusing

Healthcare billing combines:

- Deductibles

- Coinsurance

- Copays

- Network rules

- Prior authorizations

- Provider contracts

As a result, even insured patients struggle to predict actual costs.

Additionally, hospitals often send:

- Multiple bills

- Delayed invoices

- Separate physician charges

Consequently, many families underestimate their real financial responsibility.

📊 Deductible vs Coinsurance vs Copay

These three terms often overlap.

💳 Copay

Fixed amount per visit:

- Example: $25 doctor visit

📈 Coinsurance

Percentage you pay after deductible:

- Example: 20% MRI cost

🏦 Deductible

Amount you pay before insurance starts sharing costs:

- Example: first $1,500 yearly expenses

Together, these determine your actual hospital bill.

⚡ How to Reduce Your Hospital Costs

🏥 Stay In-Network

Out-of-network hospitals often create:

- Higher deductibles

- Bigger coinsurance

- Surprise bills

Therefore, always confirm network status beforehand.

📄 Review Every EOB Carefully

EOB = Explanation of Benefits.

Check:

- Billing errors

- Duplicate charges

- Incorrect coding

- Denied services

Mistakes happen more often than people realize.

💬 Negotiate Hospital Bills

Many hospitals offer:

- Financial assistance

- Payment plans

- Discounts

- Charity care

Especially for large balances.

📱 Use Cost Estimator Tools

Many insurers now provide:

- Procedure cost calculators

- In-network provider comparisons

- Hospital pricing tools

Using these tools before treatment can save enormous amounts.

🌎 What About Lifetime Maximum Benefits?

Older insurance plans sometimes included:

- Lifetime coverage caps

For example:

- $2 million maximum lifetime payout

Once exceeded:

- Insurance stopped paying entirely

However, most modern ACA-compliant plans no longer allow lifetime dollar limits on essential health benefits.

Still, some limited-benefit or supplemental plans may contain restrictions.

Therefore, reviewing policy documents remains extremely important.

🧭 Final Thoughts

Understanding deductible vs out-of-pocket maximum can completely change how you plan healthcare expenses.

The deductible determines when insurance begins helping.

Meanwhile, the out-of-pocket maximum protects you from unlimited financial exposure during serious illness or hospitalization.

Unfortunately, many Americans only learn these terms after receiving massive medical bills.

Therefore:

- Read your insurance documents carefully

- Understand your yearly limits

- Track healthcare spending

- Verify hospital network participation

Most importantly, remember this:

Having insurance does not mean healthcare becomes free — but knowing your coverage can prevent devastating surprises.

❓FAQs About Deductibles and Out-of-Pocket Maximums

What is a deductible in health insurance?

A deductible is the amount you pay for covered healthcare services before insurance starts sharing costs.

What is an out-of-pocket maximum?

It is the most you must pay yearly for covered healthcare expenses before insurance covers nearly everything else.

Does the deductible count toward the out-of-pocket maximum?

Usually, yes. Most health plans count deductible payments toward the out-of-pocket maximum.

Do copays count toward the out-of-pocket maximum?

In many plans, yes. However, policy details vary.

What happens after I meet my deductible?

Insurance begins sharing costs through coinsurance arrangements or expanded coverage benefits.

What happens after I reach my out-of-pocket maximum?

Your insurance generally pays 100% of covered in-network healthcare costs for the remainder of the year.

Do out-of-network bills count toward the maximum?

Sometimes not. Many plans exclude certain out-of-network charges.

Why do I still receive bills after meeting my deductible?

Because coinsurance, copays, non-covered services, or out-of-network charges may still apply until you hit your out-of-pocket maximum.

Authoritative Source Links

- Healthcare.gov – Deductibles, Copayments & Coinsurance

- Centers for Medicare & Medicaid Services (CMS) – Health Insurance Terms

- Kaiser Family Foundation (KFF) – Health Insurance Costs

- Investopedia – Out-of-Pocket Maximum Explained

- Blue Cross Blue Shield – Understanding Deductibles

- Cigna – Copays, Deductibles & Coinsurance Guide

You may also like to read other health related articles here also authored by me :

Gym Herpes Outbreak? How to Stay Safe While Working Out

Can Apple Cider Vinegar Help Weight Loss Journey?

Mewing Explained: Does This Viral Jawline Trend Actually Work?

What Your Hands Are Warning You About Your Heart: Hidden Signs