- COBRA vs. ACA Marketplace Cost Calculator

- 🩺 What Is COBRA?

- 💰 What Is Marketplace Health Insurance?

- 🔍 COBRA vs Marketplace: Key Differences

- 📋 COBRA vs Marketplace: Monthly Costs

- 👨⚕️ When COBRA May Be the Better Choice

- 🏥 When Marketplace Coverage May Be the Better Choice

- ⚖️ COBRA vs Marketplace for Families

- 📉 The Hidden Costs People Often Ignore

- 🚨 Common Mistakes to Avoid

- 🧠 How to Decide Between COBRA and Marketplace

- 💡 A Simple Decision Framework

- Final Thoughts on COBRA vs Marketplace

- Frequently Asked Questions (FAQs)

COBRA vs. ACA Marketplace Cost Calculator

Lost your job or changing coverage? Compare your official COBRA premium quote side-by-side with an estimated subsidized Marketplace plan.

Your COBRA Quote

Marketplace Subsidy Factors

Losing a job can feel overwhelming. Along with concerns about income, many Americans immediately worry about health insurance. After all, a single unexpected medical emergency can create thousands of dollars in expenses. Fortunately, you usually have two major options to maintain coverage: COBRA and Marketplace health insurance.

However, choosing between these options is not always straightforward. While COBRA allows you to keep your existing employer-sponsored health plan, Marketplace plans may offer lower premiums and financial assistance. Therefore, understanding the differences can help you avoid costly mistakes and secure the coverage that fits your needs.

In this comprehensive COBRA vs Marketplace guide, you'll learn how each option works, their advantages and disadvantages, and how to determine which choice makes the most sense for your situation.

🩺 What Is COBRA?

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act. It is a federal law that allows eligible employees and their families to continue their employer-sponsored health insurance after experiencing certain qualifying events.

These events may include:

- Job loss

- Reduction in work hours

- Voluntary resignation

- Divorce or legal separation

- Death of a covered employee

With COBRA, you can usually keep the exact same health plan, doctors, hospitals, and prescription drug coverage that you had while employed.

However, there is an important catch.

While your employer may have previously paid a significant portion of your premium, under COBRA you generally pay the entire premium yourself plus a small administrative fee.

As a result, many people experience sticker shock when they receive their COBRA premium notice.

💰 What Is Marketplace Health Insurance?

The Health Insurance Marketplace was established under the Affordable Care Act (ACA). It allows individuals and families to shop for health insurance plans through federal or state exchanges.

Unlike COBRA, Marketplace plans are not tied to your former employer. Instead, you can choose from multiple insurers and coverage levels.

Marketplace plans are divided into categories:

- Bronze

- Silver

- Gold

- Platinum

Each category offers different balances between monthly premiums and out-of-pocket costs.

Most importantly, many Americans qualify for premium tax credits and subsidies. Consequently, Marketplace coverage can become significantly more affordable than COBRA.

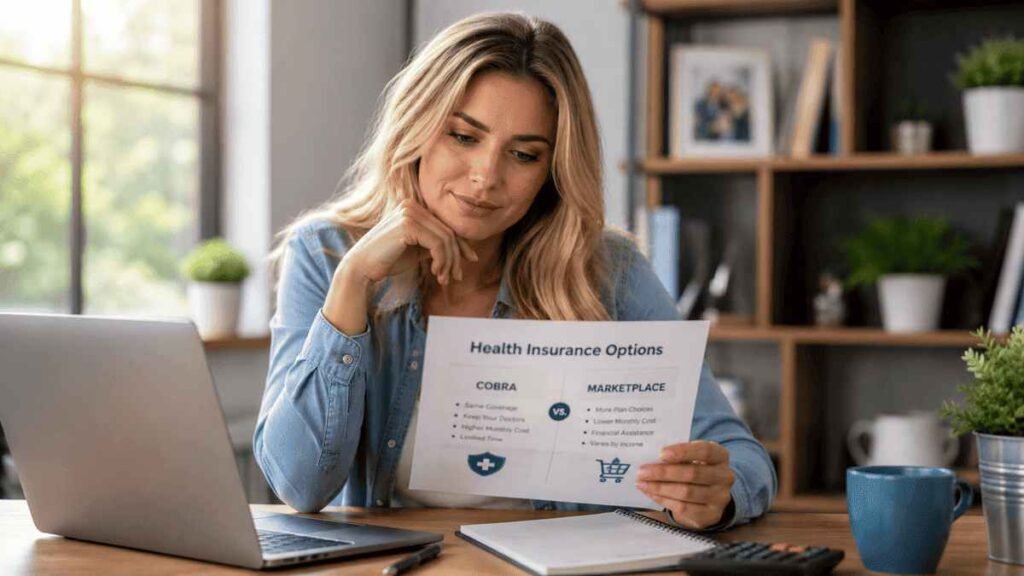

🔍 COBRA vs Marketplace: Key Differences

Understanding the major differences can make your decision easier.

| Feature | COBRA | Marketplace |

|---|---|---|

| Keeps Current Plan | Yes | No |

| Same Doctors | Usually | Depends on Network |

| Monthly Cost | Often Higher | Often Lower |

| Subsidies Available | No | Yes |

| Coverage Start | Immediate Continuation | New Policy |

| Plan Choices | Limited | Multiple Options |

| Employer Network | Same | May Change |

While both options provide valuable coverage, the right choice depends heavily on your healthcare needs and financial situation.

📋 COBRA vs Marketplace: Monthly Costs

For many households, cost becomes the deciding factor.

When employed, your company likely paid a portion of your health insurance premium. Once you elect COBRA, that employer contribution disappears.

For example:

- Employer Plan Total Cost: $900/month

- Employee Contribution While Working: $200/month

- Employer Contribution: $700/month

After electing COBRA:

- You may pay approximately $918/month including administrative fees.

As you can see, the difference can be substantial.

Meanwhile, Marketplace plans often provide premium tax credits based on household income.

Therefore, a person earning less after losing a job may qualify for significant savings.

In some cases, Marketplace coverage can cost hundreds of dollars less each month than COBRA.

👨⚕️ When COBRA May Be the Better Choice

Although COBRA can be expensive, it still offers several valuable advantages.

1. You Want to Keep Your Current Doctors

Many patients have established relationships with specialists, primary care physicians, and treatment centers.

Because COBRA continues your existing plan, you can usually keep your healthcare providers without interruption.

2. You Are Undergoing Major Treatment

If you are receiving:

- Cancer treatment

- Pregnancy care

- Dialysis

- Specialized surgeries

- Ongoing therapy

changing plans could create complications.

Consequently, many people choose COBRA temporarily until treatment concludes.

3. You Have Already Met Your Deductible

Imagine you already paid thousands toward your annual deductible.

Switching to a Marketplace plan often resets deductibles and out-of-pocket maximums.

As a result, COBRA may save money despite higher premiums.

4. You Expect to Get Another Job Soon

If you anticipate obtaining new employer-sponsored insurance within a few months, COBRA may serve as a convenient bridge.

In that situation, paying higher premiums for a short period may be worthwhile.

🏥 When Marketplace Coverage May Be the Better Choice

For many Americans, Marketplace coverage provides a more affordable solution.

1. You Need Lower Monthly Premiums

Because subsidies can dramatically reduce costs, Marketplace plans frequently offer better affordability.

Furthermore, lower premiums can ease financial pressure while you search for new employment.

2. Your Income Has Decreased

Job loss often results in lower annual income.

Therefore, you may qualify for premium tax credits that were unavailable when you were employed.

These subsidies can significantly reduce healthcare expenses.

3. You Want More Plan Options

Unlike COBRA, Marketplace coverage offers multiple insurers and plan types.

As a result, you can compare:

- Premiums

- Deductibles

- Copays

- Provider networks

- Prescription benefits

This flexibility allows you to tailor coverage to your current needs.

4. You Are Generally Healthy

If you rarely visit doctors and have minimal healthcare needs, a lower-cost Marketplace plan may provide sufficient protection.

Consequently, many healthy individuals choose Marketplace plans instead of paying expensive COBRA premiums.

⚖️ COBRA vs Marketplace for Families

Families often face additional challenges.

A family of four may encounter extremely high COBRA premiums because the employer contribution disappears for every family member.

Meanwhile, Marketplace subsidies can become especially valuable for households with moderate incomes.

Additionally, parents should evaluate:

- Pediatric care

- Prescription coverage

- Specialist access

- Emergency care networks

Before making a decision, compare total annual costs rather than focusing only on monthly premiums.

📉 The Hidden Costs People Often Ignore

Many consumers compare only monthly premiums. Unfortunately, that approach can lead to poor decisions.

Instead, examine:

Deductibles

Lower premiums often come with higher deductibles.

Copayments

Office visits, urgent care visits, and prescriptions may have different costs.

Coinsurance

You may share costs with the insurer after meeting your deductible.

Out-of-Pocket Maximums

This figure represents the most you'll pay during a policy year.

Therefore, looking beyond premiums provides a more accurate picture of total healthcare costs.

🚨 Common Mistakes to Avoid

Choosing Based Solely on Premiums

A low premium does not always equal lower overall healthcare spending.

Ignoring Provider Networks

Your preferred doctors may not participate in every Marketplace plan.

Therefore, verify network participation before enrolling.

Missing Enrollment Deadlines

Both COBRA and Marketplace coverage have strict enrollment timelines.

Consequently, delaying your decision could leave you uninsured.

Overlooking Prescription Drug Coverage

Medication costs can vary dramatically between plans.

Always review formularies before choosing coverage.

🧠 How to Decide Between COBRA and Marketplace

Ask yourself these questions:

- Do I need my current doctors?

- Have I already met my deductible?

- Am I receiving ongoing treatment?

- How much can I realistically afford each month?

- Do I qualify for Marketplace subsidies?

- Will I obtain new employer coverage soon?

If continuity of care is your highest priority, COBRA may be the better option.

On the other hand, if affordability matters most, Marketplace coverage often provides greater value.

💡 A Simple Decision Framework

Choose COBRA if You:

- want the same plan

- are in active treatment

- met most of your deductible

- expect new employment soon

Choose Marketplace if You:

- need lower monthly costs

- qualify for subsidies

- want plan flexibility

- are generally healthy

This framework won't fit every situation. Nevertheless, it can simplify the decision-making process.

Final Thoughts on COBRA vs Marketplace

Choosing health insurance after job loss can feel stressful. Nevertheless, understanding your options puts you back in control.

The COBRA vs Marketplace decision often comes down to balancing continuity and affordability. COBRA allows you to keep your existing plan and healthcare providers. Meanwhile, Marketplace coverage may offer substantial savings through premium tax credits and a wider range of plan options.

Before making a final choice, compare premiums, deductibles, provider networks, prescription coverage, and out-of-pocket maximums. Most importantly, consider your current healthcare needs and future financial goals.

A careful comparison today could save you thousands of dollars while ensuring you and your family remain protected.

Frequently Asked Questions (FAQs)

What is the biggest difference between COBRA and Marketplace insurance?

The biggest difference is that COBRA lets you keep your existing employer-sponsored health plan, while Marketplace insurance requires you to select a new plan from available insurers.

Is COBRA always more expensive than Marketplace insurance?

Not always. However, COBRA is often more expensive because you pay the full premium without employer contributions. Marketplace plans may offer subsidies that significantly lower costs.

Can I switch from COBRA to Marketplace coverage later?

Yes. Depending on your circumstances and enrollment periods, you may switch from COBRA to Marketplace coverage. Review eligibility rules carefully before making changes.

Do Marketplace plans cover pre-existing conditions?

Yes. Under the Affordable Care Act, Marketplace plans cannot deny coverage or charge higher premiums because of pre-existing conditions.

How long can I stay on COBRA?

Most people can remain on COBRA for up to 18 months after a qualifying event. Certain circumstances may allow longer coverage periods.

Can I use Marketplace subsidies if I choose COBRA?

No. Premium tax credits generally apply to Marketplace plans, not COBRA coverage.

Which option is better after losing a job?

The answer depends on your healthcare needs, finances, provider preferences, and eligibility for subsidies. Comparing total annual costs usually provides the clearest answer.

Is Marketplace coverage good enough compared to employer insurance?

Many Marketplace plans provide comprehensive coverage that includes preventive care, emergency services, hospitalization, prescriptions, and specialist care. The quality depends on the specific plan you choose.

Authoritative Sources for the Blog

Government & Official Sources

- HealthCare.gov – Marketplace Coverage Guide

- U.S. Department of Labor – COBRA Continuation Coverage

- CMS – Health Insurance Marketplace Information

- Internal Revenue Service – Premium Tax Credits

Consumer Education Sources

- KFF (Kaiser Family Foundation) – Health Insurance Explained

- Consumer Reports – Understanding Health Insurance Choices

- National Association of Insurance Commissioners (NAIC)

Additional Research Sources

- Congressional Research Service – COBRA Overview

- Commonwealth Fund – Health Insurance Coverage Research

You may also like to read other health related articles here also authored by me :

- Best Lawyer for Health Insurance Denial in Florida: Win Your Claim

- Judge Blocks Trump SNAP Funding Restrictions

- Your Health Insurance Said “NO”? Here’s What To Do

- Plant Protein vs Animal Protein: What’s Best for You?

- 5 Best Cancer Hospitals in Texas (2026 Comparison & Rankings)

- 24-Year-Old Texas Nurse Suffers Shocking Stroke

- 3 Day Fix to Reverse Fatty Liver Fast: A Simple Reset